import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import xgboost as xgbXGBoost for Regression in Python

python

tutorial

gradient boosting

xgboost

A step-bystep tutorial on regression with XGBoost in python using sklearn and the xgboost library

In this post I’m going to show you my process for solving regression problems with XGBoost in python, using either the native xgboost API or the scikit-learn interface. This is a powerful methodology that can produce world class results in a short time with minimal thought or effort. While we’ll be working on an old Kagle competition for predicting the sale prices of bulldozers and other heavy machinery, you can use this flow to solve whatever tabular data regression problem you’re working on.

This post serves as the explanation and documentation for the XGBoost regression jupyter notebook from my ds-templates repo on GitHub, so go ahead and download the notebook and follow along with your own data.

If you’re not already comfortable with the ideas behind gradient boosting and XGBoost, you’ll find it helpful to read some of my previous posts to get up to speed. I’d start with this introduction to gradient boosting, and then read this explanation of how XGBoost works.

Let’s get into it! 🚀

Install and import the xgboost library

If you don’t already have it, go ahead and use conda to install the xgboost library, e.g.

$ conda install -c conda-forge xgboostThen import it along with the usual suspects.

Read dataset into python

In this example we’ll work on the Kagle Bluebook for Bulldozers competition, which asks us to build a regression model to predict the sale price of heavy equipment. Amazingly, you can solve your own regression problem by swapping this data out with your organization’s data before proceeding with the tutorial.

Go ahead and download the Train.zip file from Kagle and extract it into Train.csv. Then read the data into a pandas dataframe.

df = pd.read_csv('Train.csv', parse_dates=['saledate']);Notice I cheated a little bit, checking the columns ahead of time and telling pandas to treat the saledate column as a date. In general it will make life easier to read in any date-like columns as dates.

df.info()<class 'pandas.core.frame.DataFrame'>

RangeIndex: 401125 entries, 0 to 401124

Data columns (total 53 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 SalesID 401125 non-null int64

1 SalePrice 401125 non-null int64

2 MachineID 401125 non-null int64

3 ModelID 401125 non-null int64

4 datasource 401125 non-null int64

5 auctioneerID 380989 non-null float64

6 YearMade 401125 non-null int64

7 MachineHoursCurrentMeter 142765 non-null float64

8 UsageBand 69639 non-null object

9 saledate 401125 non-null datetime64[ns]

10 fiModelDesc 401125 non-null object

11 fiBaseModel 401125 non-null object

12 fiSecondaryDesc 263934 non-null object

13 fiModelSeries 56908 non-null object

14 fiModelDescriptor 71919 non-null object

15 ProductSize 190350 non-null object

16 fiProductClassDesc 401125 non-null object

17 state 401125 non-null object

18 ProductGroup 401125 non-null object

19 ProductGroupDesc 401125 non-null object

20 Drive_System 104361 non-null object

21 Enclosure 400800 non-null object

22 Forks 192077 non-null object

23 Pad_Type 79134 non-null object

24 Ride_Control 148606 non-null object

25 Stick 79134 non-null object

26 Transmission 183230 non-null object

27 Turbocharged 79134 non-null object

28 Blade_Extension 25219 non-null object

29 Blade_Width 25219 non-null object

30 Enclosure_Type 25219 non-null object

31 Engine_Horsepower 25219 non-null object

32 Hydraulics 320570 non-null object

33 Pushblock 25219 non-null object

34 Ripper 104137 non-null object

35 Scarifier 25230 non-null object

36 Tip_Control 25219 non-null object

37 Tire_Size 94718 non-null object

38 Coupler 213952 non-null object

39 Coupler_System 43458 non-null object

40 Grouser_Tracks 43362 non-null object

41 Hydraulics_Flow 43362 non-null object

42 Track_Type 99153 non-null object

43 Undercarriage_Pad_Width 99872 non-null object

44 Stick_Length 99218 non-null object

45 Thumb 99288 non-null object

46 Pattern_Changer 99218 non-null object

47 Grouser_Type 99153 non-null object

48 Backhoe_Mounting 78672 non-null object

49 Blade_Type 79833 non-null object

50 Travel_Controls 79834 non-null object

51 Differential_Type 69411 non-null object

52 Steering_Controls 69369 non-null object

dtypes: datetime64[ns](1), float64(2), int64(6), object(44)

memory usage: 162.2+ MBPrepare raw data for XGBoost

When faced with a new tabular dataset for modeling, we have two format considerations: data types and missingness. From the call to df.info() above, we can see we have both mixed types and missing values.

When it comes to missing values, some models like the gradient booster or random forest in scikit-learn require purely non-missing inputs. One of the great strengths of XGBoost is that it relaxes this requirement, allowing us to pass in missing feature values, so we don’t have to worry about them.

Regarding data types, all ML models for tabular data require inputs to be numeric, either integers or floats, so we’re going to have to deal with those object columns.

Encode string features

The simplest way to encode string variables is to map each unique string value to an integer; this is called integer encoding.

We can easily accomplish this by using the categorical data type in pandas. The category type is a bit like the factor type in R; pandas stores the underlying data as integers, and it keeps a mapping from the integers back to the original string values. XGBoost is able to access the numeric data underlying the categorical features for model training and prediction. This is a nice way to encode string features because it’s easy to implement and it preserves the original category levels in the data frame. If you prefer to generate your own integer mappings, you can also do it with the scikit-learn OrdinalEncoder.

def encode_string_features(df):

out_df = df.copy()

for feature, feature_type in df.dtypes.items():

if feature_type == 'object':

out_df[feature] = out_df[feature].astype('category')

return out_df

df = encode_string_features(df)Encode date and timestamp features

While dates feel sort of numeric, they are not quite numbers, so we need to transform them into numeric columns that XGBoost can understand. Unfortunately, encoding timestamps isn’t as straightforward as encoding strings, so we actually might need to engage in a little bit of feature engineering. A single date has many different attributes, e.g. days since epoch, year, quarter, month, day, day of year, day of week, is holiday, etc. Often a simple time index is the most useful information in a date column, so here we’ll just start by adding a feature that gives the number of days since some epoch date.

df['saledate_days_since_epoch'] = (

df['saledate'] - pd.Timestamp(year=1970, month=1, day=1)

).dt.daysTransform the target if necessary

In the interest of speed and efficiency, we didn’t bother doing any EDA with the feature data. Part of my justification for this is that trees are incredibly robust to outliers, colinearity, missingness, and other assorted nonsense in the feature data. However, they are not necessarily robust to nonsense in the target variable, so it’s worth having a look at it before proceeding any further.

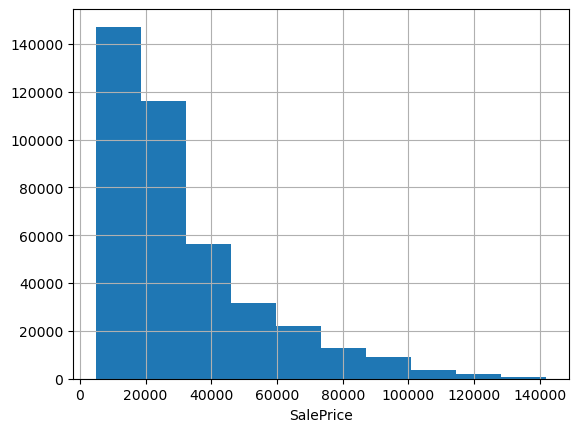

df.SalePrice.hist(); plt.xlabel('SalePrice');

Often when predicting prices it makes sense to use log price, especially when they span multiple orders of magnitude or have a strong right skew. These data look pretty friendly, lacking outliers and exhibiting only a mild positive skew; we could probably get away without doing any transformation. But checking the evaluation metric used to score the Kagle competition, we see they’re using root mean squared log error. That’s equivalent to using RMSE on log-transformed target data, so let’s go ahead and work with log prices.

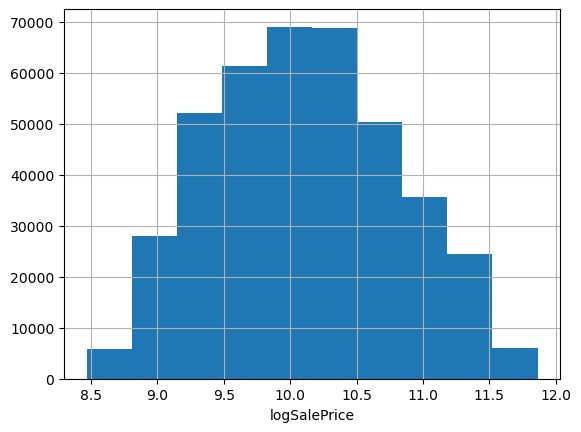

df['logSalePrice'] = np.log1p(df['SalePrice'])

df.logSalePrice.hist(); plt.xlabel('logSalePrice');

Train and Evaluate the XGBoost regression model

Having prepared our dataset, we are now ready to train an XGBoost model. Let’s walk through the flow step-by-step.

Split the data into training and validation sets

First we split the dataset into a training set and a validation set. Of course since we’re going to evaluate against the validation set a number of times as we iterate, it’s best practice to keep a separate test set reserved to check our final model to ensure it generalizes well. Assuming that final test set is hidden away, we can use the rest of the data for training and validation.

There are two main ways we might want to select the validation set. If there isn’t a temporal ordering of the observations, we might be able to randomly sample. In practice, it’s common that observations have a temporal ordering, and that models are trained on observations up to a certain time and used to predict on observations occuring after that time. Since this data is temporal, we don’t want to split randomly; instead we’ll split on observation date, reserving the latest observations for the validation set.

# Temporal Validation Set

def train_test_split_temporal(df, datetime_column, n_test):

idx_sort = np.argsort(df[datetime_column])

idx_train, idx_test = idx_sort[:-n_valid], idx_sort[-n_valid:]

return df.iloc[idx_train, :], df.iloc[idx_test, :]n_valid = 12000

train_df, valid_df = train_test_split_temporal(df, 'saledate', n_valid)

train_df.shape, valid_df.shape((389125, 55), (12000, 55))Specify target and feature columns

Next we’ll put together a list of our features and define the target column. I like to have an actual list defined in the code so it’s easy to explicitly see everything we’re puting into the model and easier to add or remove features as we iterate. Just run something like list(df.columns) in a cel to get a copy-pasteable list of columns, then edit it down to the full list of features, i.e. remove the target, date columns, and other non-feature columns..

# list(df.columns)features = [

'SalesID',

'MachineID',

'ModelID',

'datasource',

'auctioneerID',

'YearMade',

'MachineHoursCurrentMeter',

'UsageBand',

'fiModelDesc',

'fiBaseModel',

'fiSecondaryDesc',

'fiModelSeries',

'fiModelDescriptor',

'ProductSize',

'fiProductClassDesc',

'state',

'ProductGroup',

'ProductGroupDesc',

'Drive_System',

'Enclosure',

'Forks',

'Pad_Type',

'Ride_Control',

'Stick',

'Transmission',

'Turbocharged',

'Blade_Extension',

'Blade_Width',

'Enclosure_Type',

'Engine_Horsepower',

'Hydraulics',

'Pushblock',

'Ripper',

'Scarifier',

'Tip_Control',

'Tire_Size',

'Coupler',

'Coupler_System',

'Grouser_Tracks',

'Hydraulics_Flow',

'Track_Type',

'Undercarriage_Pad_Width',

'Stick_Length',

'Thumb',

'Pattern_Changer',

'Grouser_Type',

'Backhoe_Mounting',

'Blade_Type',

'Travel_Controls',

'Differential_Type',

'Steering_Controls',

'saledate_days_since_epoch'

]

target = 'logSalePrice'Create DMatrix data objects

XGBoost uses a data type called dense matrix for efficient training and prediction, so next we need to create DMatrix objects for our training and validation datasets. Remember how we decided to encode our string columns by casting them as pandas categorical types? For this to work, we need to set the enable_categoricals argument to True.

dtrain = xgb.DMatrix(data=train_df[features], label=train_df[target],

enable_categorical=True)

dvalid = xgb.DMatrix(data=valid_df[features], label=valid_df[target],

enable_categorical=True)Set the XGBoost parameters

XGBoost has numerous hyperparameters. Fortunately, just a handful of them tend to be the most influential; furthermore, the default values are not bad in most situations. I like to start out with a dictionary containing the default values for the parameters I’m most likely to adjust later, with one exception. I dislike the default value of auto for the tree_method parameter, which tells XGBoost to choose a tree method on it’s own. I’ve been burned by this ambiguity in the past, so now I prefer to set it to approx. For training there is one required boosting parameter called num_boost_round which I set to 50 as a starting point.

# default values for important parameters

params = {

'tree_method': 'approx',

'learning_rate': 0.3,

'max_depth': 6,

'min_child_weight': 1,

'subsample': 1,

'colsample_bynode': 1,

'objective': 'reg:squarederror',

}

num_boost_round = 50Train the XGBoost model

The xgb.train() function takes our training dataset and parameters, and it returns a trained XGBoost model, which is an object of class xgb.core.Booster. Check out the documentation on the learning API to see all the training options. During training, I like to have XGBoost print out the evaluation metric on the train and validation set after every few boosting rounds and again at the end of training; that can be done by setting evals and verbose_eval.

model = xgb.train(params=params, dtrain=dtrain, num_boost_round=num_boost_round,

evals=[(dtrain, 'train'), (dvalid, 'valid')],

verbose_eval=10)[0] train-rmse:6.74240 valid-rmse:6.80825

[10] train-rmse:0.31071 valid-rmse:0.34532

[20] train-rmse:0.21950 valid-rmse:0.24364

[30] train-rmse:0.20878 valid-rmse:0.23669

[40] train-rmse:0.20164 valid-rmse:0.23254

[49] train-rmse:0.19705 valid-rmse:0.23125Train the XGBoost model using the sklearn interface

If you prefer scikit-learn-like syntax, you can use the sklearn estimator interface to create and train XGBoost models. The XGBRegressor class, which is available in the xgboost library that we already imported, constructs an XGBRegressor object with fit and predict methods like you’re used to using in scikit-learn. The fit and predict methods take pandas dataframes, so you don’t need to create DMatrix data objects yourself; however, since these methods still have to transform input data into DMatrix objects internally, training and prediction seem to be slower via the sklearn interface.

# scikit-learn interface

reg = xgb.XGBRegressor(n_estimators=num_boost_round, enable_categorical=True, **params)

reg.fit(train_df[features], train_df[target],

eval_set=[(train_df[features], train_df[target]), (valid_df[features], valid_df[target])],

verbose=10);[0] validation_0-rmse:6.74240 validation_1-rmse:6.80825

[10] validation_0-rmse:0.31071 validation_1-rmse:0.34532

[20] validation_0-rmse:0.21950 validation_1-rmse:0.24364

[30] validation_0-rmse:0.20878 validation_1-rmse:0.23669

[40] validation_0-rmse:0.20164 validation_1-rmse:0.23254

[49] validation_0-rmse:0.19705 validation_1-rmse:0.23125Since not all features of XGBoost are available through the scikit-learn estimator interface, you might want to get the native xgb.core.Booster object back out of the sklearn wrapper.

booster = reg.get_booster()Evaluate the XGBoost model and check for overfitting

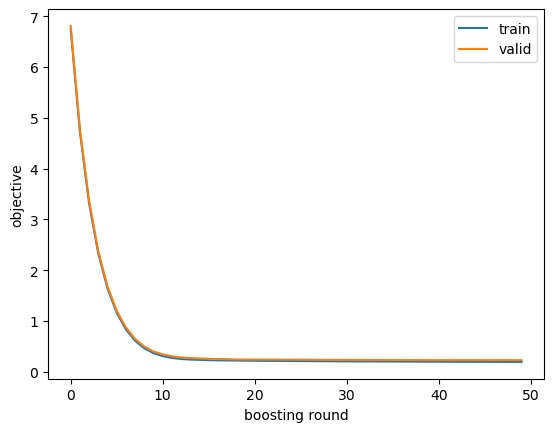

We get the model evaluation metrics on the training and validation sets printed to stdout when we use the evals argument to the training API. Typically I just look at those printed metrics, but sometimes it’s helpful to retain them in a variable for further inspection via, e.g. plotting. To do that we need to train again, passing an empty dictionary to the evals_result argument. In the objective curves, I’m looking for signs of overfitting, which could include validation scores staying the same or getting worse over later iterations or huge gaps between training and validation scores.

evals_result = {}

model = xgb.train(params=params, dtrain=dtrain, num_boost_round=num_boost_round,

evals=[(dtrain, 'train'), (dvalid, 'valid')],

verbose_eval=10,

evals_result=evals_result)[0] train-rmse:6.74240 valid-rmse:6.80825

[10] train-rmse:0.31071 valid-rmse:0.34532

[20] train-rmse:0.21950 valid-rmse:0.24364

[30] train-rmse:0.20878 valid-rmse:0.23669

[40] train-rmse:0.20164 valid-rmse:0.23254

[49] train-rmse:0.19705 valid-rmse:0.23125pd.DataFrame({

'train': evals_result['train']['rmse'],

'valid': evals_result['valid']['rmse']

}).plot(); plt.xlabel('boosting round'); plt.ylabel('objective');

While we could just look at the validation RMSE in the printed output from model training, let’s go ahead and compute it by hand, just to be sure.

from sklearn.metrics import mean_squared_error

# squared=False returns RMSE

mean_squared_error(y_true=dvalid.get_label(),

y_pred=model.predict(dvalid),

squared=False)0.23124987So, how good is that RMSLE of 0.231? Well, checking the Kagle leaderboard for this competition, we would have come in around 5th out of 474. That’s not bad for 10 minutes of work doing the bare minimum necessary to transform the raw data into a format consumable by XGBoost and then training a model using default hyperparameter values. To improve our model from here we would want to explore some feature engineering and some hyperparameter tuning, which we’ll save for another post.

Wait, why was that so easy? Since XGBoost made it’s big Kagle debut in the 2014 Higgs Boson competition, presumably no one in this 2013 competition was using it yet. A second potential reason is that we’re using a different validation set from that used for the final leaderboard (which is long closed), but our score is likely still a decent approximation for how we would have done in the competition.

XGBoost Model Interpretation

Next let’s have a look at how to apply a couple of the most common model interpretation techniques, feature importance and partial dependence, to XGBoost.

Remember we have two trained models floating around: one called

modelof classxgb.core.Boosterwhich is compatible with xgboost library utilities and another calledregof classXGBRegressorwhich is compatible with scikit-learn utilities. We need to be sure to use the model that’s compatible with whatever utility we’re using.

While these interpretation tools are still very common, there’s a newer, more comprehensive, and self-consistent model interpretation framework called SHAP that’s worth checking out.

Feature Importance for XGBoost

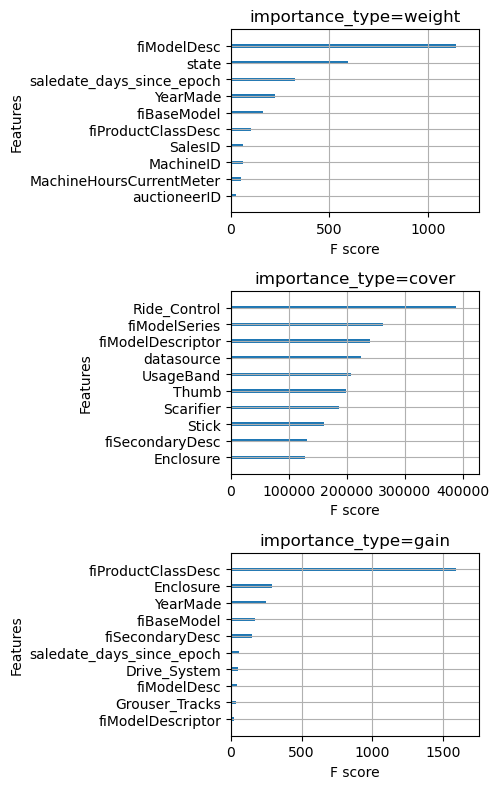

While XGBoost automatically computes feature importance by three different metrics during training, you should only use them with great care and skepticism. The three metrics are

- weight: the number of splits that use the feature

- gain: the average gain in the objective function from splits which use the feature

- cover: the average number of training samples affected by splits that use the feature

The first problem with these metrics is that they are computed using only the training dataset, which means they don’t reflect how useful a feature is when predicting on out-of-sample data. If your model is overfit on some nonsense feature, it will still have a high importance. Secondly, I think they are difficult to interpret; all three are specific to decision trees and reflect domain-irrelevant idiosyncrasies like whether a feature is used nearer the root or the leaves of a tree. Anyway let’s see what these metrics have to say about our features.

fig, (ax1, ax2, ax3) = plt.subplots(3, 1, figsize=(5, 8))

xgb.plot_importance(model, importance_type='weight', title='importance_type=weight',

max_num_features=10, show_values=False, ax=ax1, )

xgb.plot_importance(model, importance_type='cover', title='importance_type=cover',

max_num_features=10, show_values=False, ax=ax2)

xgb.plot_importance(model, importance_type='gain', title='importance_type=gain',

max_num_features=10, show_values=False, ax=ax3)

plt.tight_layout()

Wow, notice that the top 10 features by weight and by cover are completely different. This should forever cause you to feel skeptical whenever you see a feature importance plot.

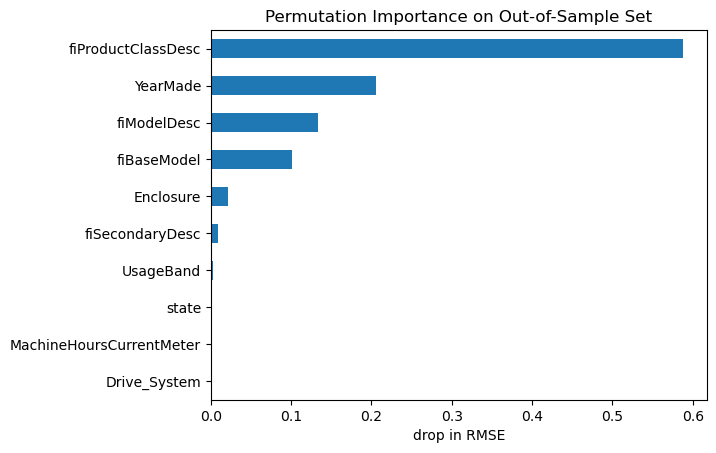

Luckily, there is a better way. IMHO, permutation feature importance is better aligned with our intuition about what feature importance should mean. It tells us by how much the model performance decreases when the values of a particular feature are randomly shuffled during prediction. This effectively breaks the relationship between the feature and the target, thus revealing how much the model relies on that feature for prediction. It also has the benefit that it can be computed using either training data or out-of-sample data.

from sklearn.inspection import permutation_importance

from sklearn.metrics import make_scorer

# make a scorer for RMSE

scorer = make_scorer(mean_squared_error, squared=False)

permu_imp = permutation_importance(reg, valid_df[features], valid_df[target],

n_repeats=30, random_state=0, scoring=scorer)importances_permutation = pd.Series(-1 * permu_imp['importances_mean'], index=features)

importances_permutation.sort_values(ascending=True)[-10:].plot.barh()

plt.title('Permutation Importance on Out-of-Sample Set')

plt.xlabel('drop in RMSE');

Now we can see which features the model relies on most for out-of-sample predictions. These are good candidate features to dig into with some EDA and conversations with any domain expert collaborators.

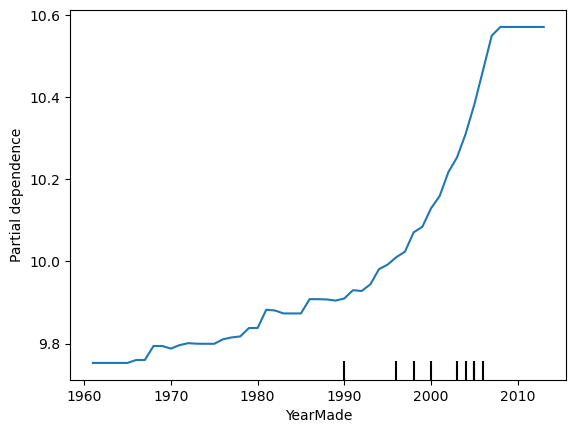

Partial Dependence Plots for XGBoost

A partial dependence plot (PDP) is a representation of the dependence between the target variable and one or more feature variables. We can loosely interpret it as showing how the expected value of the target changes across values of a particular feature, marginalizing over other features. I say “loosely” because it comes with caveats, a particularly serious one being that correlation among features tends to invalidate the above interpretation. Anyway, we can treat PDPs as useful heuristics for getting a sense of how a model thinks the target changes with feature values.

from sklearn.inspection import PartialDependenceDisplay

PartialDependenceDisplay.from_estimator(reg,

valid_df[features].query('YearMade >= 1960'),

['YearMade']);

It looks like the log sale price tends to increase in a non-linear way with year made.

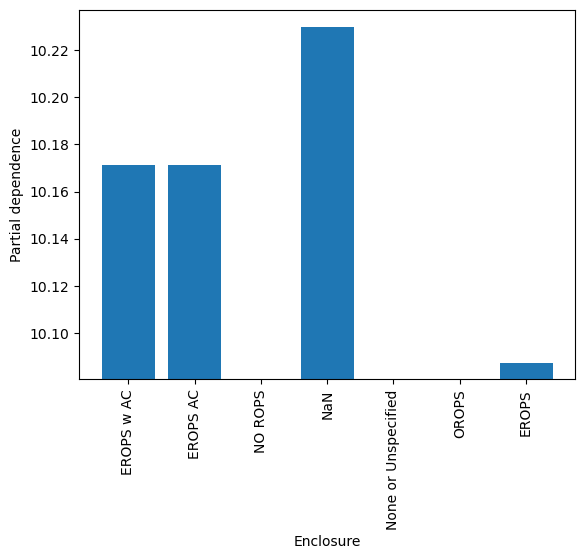

Code

# The PDPs for categorical features expect numeric data, not pandas categorical types,

# so the sklearn API for partial dependence won't work directly with the dataframe we've been using.

# The workaround is to create a new dataframe where categorical columns are encoded numerically,

# retrain the XGBoost model using the sklearn interface, create the PDPs,

# then add the category levels as the tick labels for the PDP.

def cat_pdp():

cat_feature = 'Enclosure'

modified_df = df.copy()

cat_codes = modified_df[cat_feature].cat.codes

cat_labels = list(modified_df[cat_feature].cat.categories)

cat_labels = ['NaN'] + cat_labels if -1 in cat_codes.unique() else cat_labels

modified_df[cat_feature] = cat_codes

n_valid = 12000

train_df, valid_df = train_test_split_temporal(modified_df, 'saledate', n_valid)

train_df.shape, valid_df.shape

# scikit-learn interface

reg = xgb.XGBRegressor(n_estimators=num_boost_round, enable_categorical=True, **params)

reg.fit(train_df[features], train_df[target],

eval_set=[(train_df[features], train_df[target]), (valid_df[features], valid_df[target])],

verbose=0);

PartialDependenceDisplay.from_estimator(reg, valid_df[features], [cat_feature], categorical_features=[cat_feature])

plt.xticks(ticks=cat_codes.unique(), labels=cat_labels)

cat_pdp()

You can imagine how useful these model interpretation tools can be, both for understanding data and for improving your models.

Wrapping Up

There you have it, a simple flow for solving regression problems with XGBoost in python. Remember you can use the XGBoost regression notebook from my ds-templates repo to make it easy to follow this flow on your own problems. If you found this helpful, or if you have additional ideas about solving regression problems with XGBoost, let me know down in the comments.